Of Interest: 09.21.2023

Perhaps one of the biggest market surprises of 2023 has been the relative sturdiness of the U.S. economy in the face of 550 basis points of rate increases, as well as a mildly serious (albeit short) banking crisis. This economy continues to confound bond bulls who have secretly been wishing for a sharp decline in the economy and/or some type of credit event. Either of these scenarios would potentially force the Fed into rate cutting mode. We emphasize “potentially”, because it’s far from convincing as to whether they possess the flexibility they once did. The reason for this is simple…inflation and inflationary expectations will continue to remain problematic.

We firmly believe that it is far from a coincidence that bond and equity markets have been on wildly divergent paths post-SVB’s demise. The willingness of the Fed to pull one more bailout out of their trick bag, even with inflation remaining problematic, shows their true resolve is conditional. While it is feasible that a downturn, if severe enough, will force the Fed into an easing mode, this has to be tempered with the fact that recessionary forces do not always equate with a permanent dampening of inflation.

The Fed would do well to read the latest IMF working paper, which looked at 100 separate inflation shocks in 56 countries since the 1970’s. Inflation was “resolved” in 60% of the cases, and in those cases where it was unresolved they typically involved “premature celebrations”. These mission accomplished moments are attributed to situations where inflation declined initially, only to “plateau at an elevated level or re-accelerate”. The report also goes on to mention that it “found no statistically significant difference in growth outcomes between countries that resolved inflation and those that did not. ….the mean and median output declines are marginally larger for unresolved episodes over the medium term”.

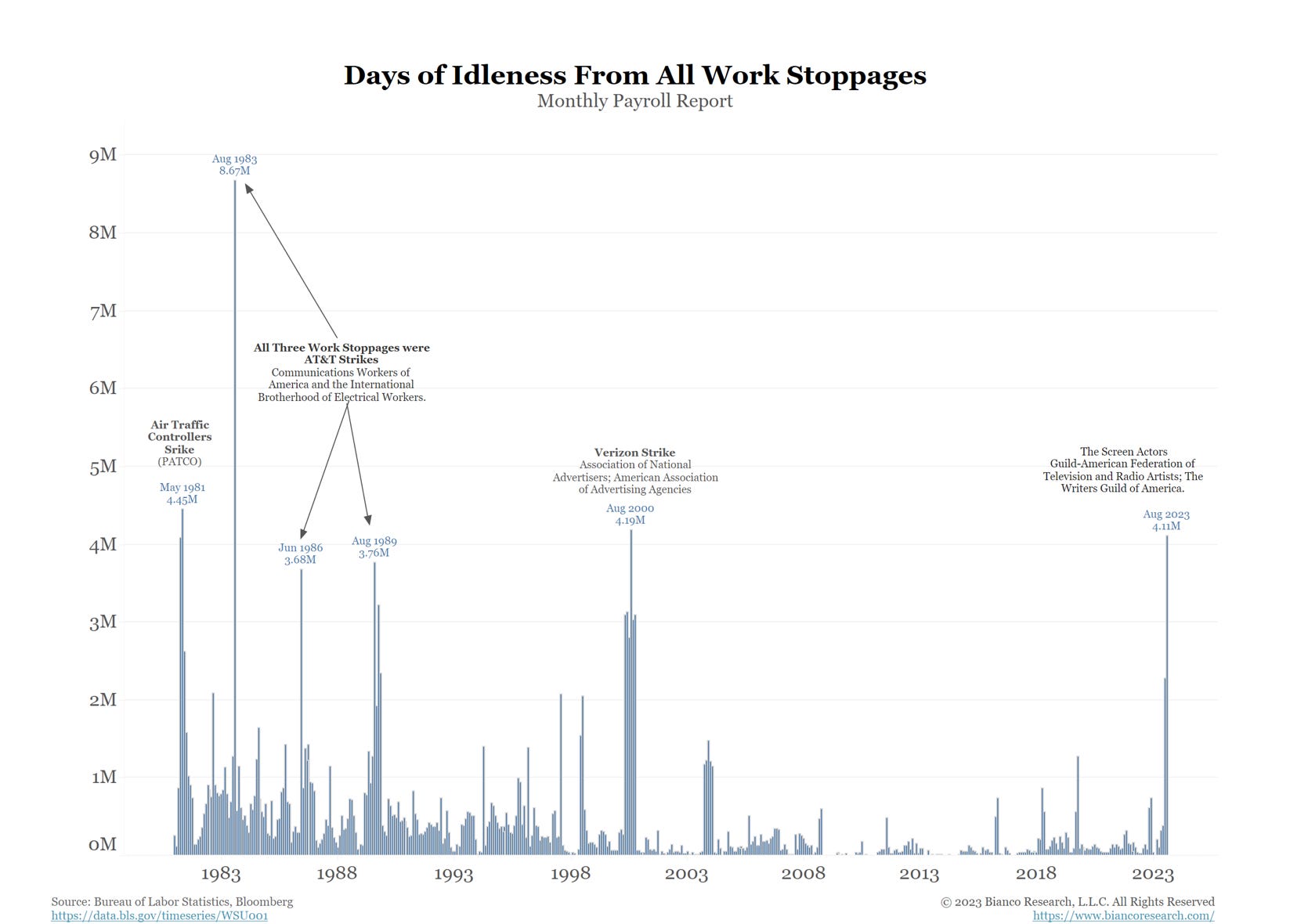

Thus, not only is the Fed not getting the downturn it so desperately wants, historically the data shows that a permanent resolution in elevated inflation is not guaranteed by either declines in employment or economic output. This is key as the labor market has clearly been paying attention to what is happening on the inflation front. The current environment involves the highest amount of labor disputes as measured by worker days lost than any period over the last 25 years. As we pointed out here, these contract agreements generally cover a term of three years or longer, which means that the inflationary expectations that the Fed is so intent on manipulating are already getting built into labor costs regardless of future policy moves.

The Fed wrapped up its two-day meetings this past Wednesday with the much anticipated (99% probability) decision to hold rates steady. The reasoning behind a ridiculously termed “hawkish hold” strategy can only be described as puzzling. Why would the Fed pause when, by our account, the potential for inflation to re-accelerate is at least as great as the potential for it to continue its descent? That is a large part of why the Treasury curve has stayed deeply inverted for so long.

Takeaways: Forget what the financial press tells you about the shape of the yield curve. Its deep, sustained inversion is telling you one thing: The bond market does not trust the Fed. The willingness to maintain a restrictive policy with the end goal of taming inflation is wholly conditional. The conditions that would preempt this “tight” money policy are already baked in this distrust…i.e. recession, credit event/mishap, external shock, etc.