Of Interest: 04.18.2024

It’s getting crowded in SOP’s tent as more and more are coming around to our long-standing belief that rates will stay higher for longer commensurate with a stickier than expected rate of inflation. The market itself has been consistently at odds with stated Fed policy over the past 8-12 months, with its optimism on rate cuts mostly driven by the belief that the economy was on the precipice of a recession that has yet to materialize (or has already come and left).

We continue to question why rate cuts are being discussed at all given where inflation is. The answer is one that is not all that surprising since we're in an election cycle, however it should be concerning given that the Fed’s credibility is once again being called into question.

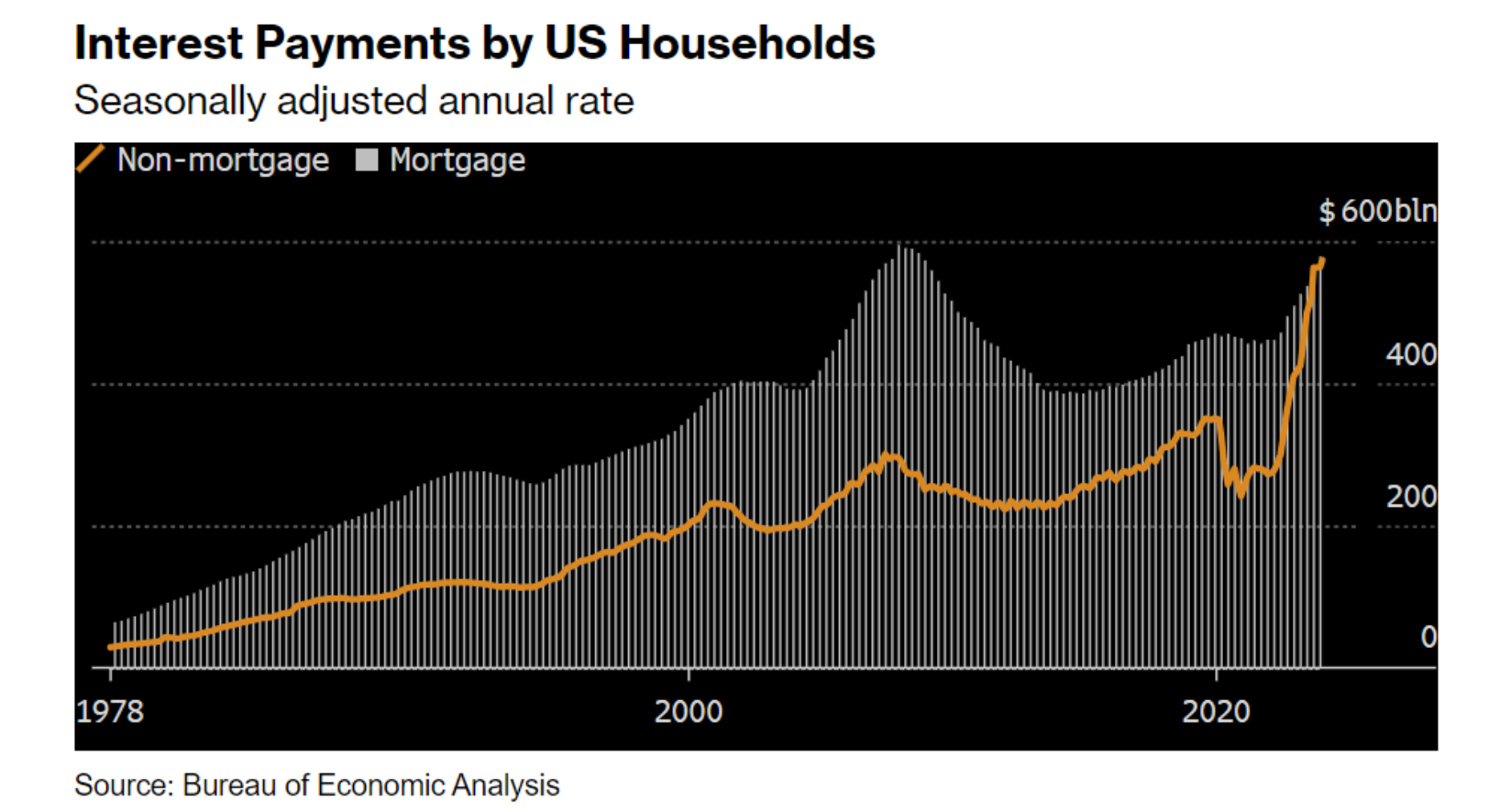

While it would appear on the surface that the Fed’s rapid increase in rates has brought little harm to the broader economy, as evidenced by the capital markets, the reality is that increased financing for the broader populace has been extensive. The graph below shows that non-mortgage interest costs have now caught up with total mortgage financing costs, which means that credit card and auto loan rates have experienced meaningful jumps. Charts like this, in addition to prices at the pump, get you voted out of office.

Anyone who has insurance coverage, particularly automobile, will have noticed the substantial increase in rates of late. One of the reasons provided for the insurance spike is a line item termed “social inflation”. Social inflation is a cost that the insurance companies are now offloading onto their policyholders resulting from the many class action lawsuits that have materialized over the last few years (and just now being settled due to Covid delays). In effect, the social “justice” being meted out in the courtrooms is now being borne by policyholders.

Any attempts by the Fed to lower rates, with inflation still very much at troublesome levels, suggests that they are at real risk of damaging the progress already made. In fact, we posit that any new spark in inflation should be attributed to this new kind of “social inflation”, whereby policy is being dictated by political ends and not the data. We doubt however that politicians (or the Fed) will embrace this new term like they have with greedflation and/or shrinkflation.

At the onset of the curve inversion we expressed our belief that the cause was a direct result of the market’s unwillingness to believe that the Fed would stay the course. The inversion was not, as most market participants believed, a precursor or predeterminate of a recession, but instead represented a gauge for how tight the market felt the Fed should remain. This is borne out in the behavior of the curve during potential credit events, including SVB and the more recent hiccup with NYCB. In both cases, short rates plummeted only to snap right back.

As markets begin to reprice based on the persistence and possible reigniting of inflationary pressures, some are now calling for the possibility of a rate increase (as we suggested long ago in an earlier commentary). In fact, strategists at UBS have stated that we may be looking at a Fed Funds rate of 6.5% by mid-2025.

Takeaways: Markets have pivoted away from Chairman Powell’s inexplicable rate-cut comments from early-December and have priced out almost all Fed action in 2024. We remain steadfast in our prediction that the natural rate of interest for the 10-Year Treasury is, at a minimum, 5.5% given our outlook on growth and inflation.