Expensive Strippers

Expensive Strippers

Weekly Commodity Roundup 02.09.2024

Macro-Economic Environment

The promise of artificial intelligence has brought into question the actual intelligence of those buyers that would bid stocks like NVDA to such lofty valuations. While some may argue that parts of the tech sector are not that overdone on an absolute basis, on a relative basis they are starting to reach historic proportions. At current valuations, the market capitalization of NVDA exceeds the market capitalization of the entire U.S. energy sector (producers). Even when looking more broadly, the S&P 500 has vastly outperformed the commodity markets. Why are commodities so unloved, and is this 2nd-Class status justified?

We believe (as we first outlined in our “Of Interest” publication) that part of the aversion towards commodities is due to the severe underperformance of both the Chinese economy and the Chinese equity markets. From our perspective, capital markets are using the decline of Chinese equities as a proxy for falling commodity demand. Given the severe decline in Chinese markets over the last several quarters, it seems like a reasonable narrative. While it is true that China is the marginal buyer for almost all commodities worldwide, the persistent selling across the entire complex is widely overdone.

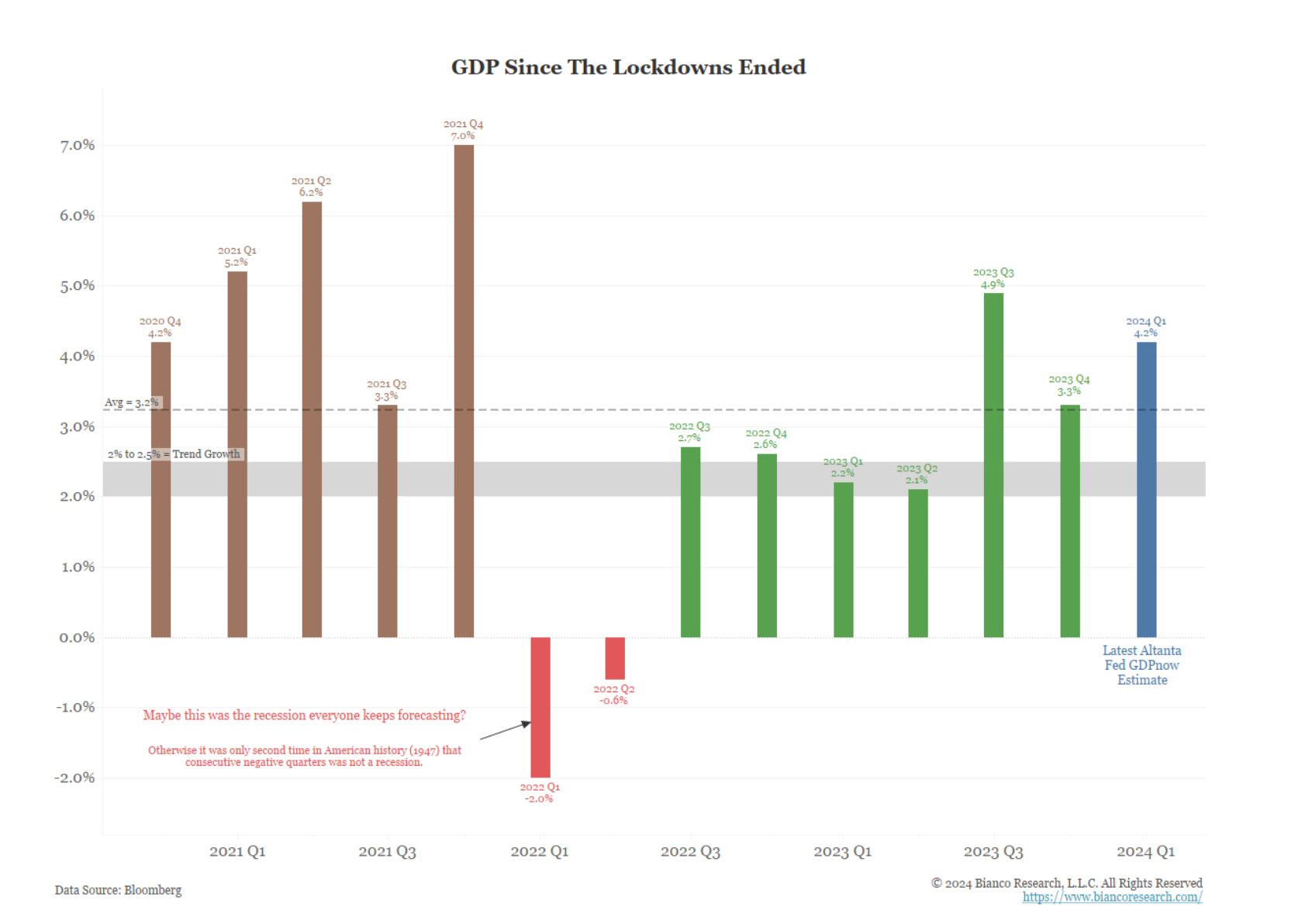

Recessionary concerns provide another potential shock to the markets that have allowed commodities sellers to maintain the upper hand for most of the last 12-14 months. While such tried and true indicators such as an inverted yield curve have been signaling (falsely thus far) a recession for over a year, it is difficult to find forward-looking indicators suggesting an imminent slowdown. In fact, we are tending to side with Jim Bianco of Bianco Research who believes that the recession already (albeit briefly) occurred back in 2022. If this is the case, future commodity demand is being vastly underpriced.

At this stage in the equity bull market, gravity begins to exert a strong force on prices, and even solid fundamentals are not sufficient to keep prices aloft. In periods like we are presently in, narratives tend to keep the party going and it is not a coincidence that AI became the next “new story” right around the market lows of June 2023. The oil supermajors (Exxon, Chevron, Shell, Total and BP) returned $113 Billion to shareholders via buybacks and dividends in 2023, 76% more than in the period spanning 2011-2014 when oil was above the $100/barrel mark. This is widely ignored in the equity markets, however, where oil stocks trade at roughly a 40% discount to the market multiple.

We have spent our entire careers in commodity markets and this “nobody’s home” feel to commodities and commodity-related equities is nothing new. We’ve seen this movie played out in 1994, 2000-2002, and again in 2007-2009. Our experience has shown that most “shocks” are attributed to the demand side, coincident with an unexpected economic downturn. Today’s environment is unique in that the markets have already anticipated (rightly or wrongly) the demand declines. Therefore, any surprises or shocks will arise as a result of insufficient supply (much like we saw in the pandemic).

Takeaways: The imbalances in equity markets are emblematic of the disparities that we are witnessing across other sectors, namely commodities. The singularly-focused narrative that is driving the “Mag 7” ever-higher is similarly driving the commodity sector lower…and towards greater opportunities.

Commodities/Energy

We have previously discussed ongoing consolidation within the domestic upstream (E&P) sector in numerous commentaries. Most of the color surrounding recent acquisitions was centered around acreage/location optimization with synergistic attributes. In fact, another tie-up was announced this week with California Resources merging with Aera Energy in a $2.1Bn (all stock) transaction. However, there is another underlying reason independent producers are increasingly falling away, and it’s attributed not to their assets, but rather their (future) liabilities.

A bevy of new regulations are coming through in 2024 and beyond that makes the cost of adherence to these rules, in many instances, no longer economic. Updated mandates range from ongoing methane monitoring to the plugging of wells. According to Enverus, their base case assumes there are ~572K non-orphaned wells potentially at risk from strained single-well economics or from operator solvency, with plugging costs totaling $32Bn. Adding the plugging of state-estimated orphaned wells increases the total to $42Bn.

To further complicate the matter, there are differences in interpretation regarding how smaller operators are to be treated. In short, operators emitting no more than 25,000 metric tons of CO2 per facility were thought to be exempt through language embedded in the IRA. However, the EPA’s most recent interpretation defines a facility as all of the operator’s wells within an entire Basin. No matter how you slice it, the cost of doing business is rising…to uneconomic levels for many. For the thousands of “stripper” well owners out there, this is an expensive regulatory lap dance.

While we are on the subject of higher fees, navigating through the Red Sea and “The Gate of Tears” has resulted in just that. Prior to the Hamas attacks in early-October, it has been estimated that about 11% of world trade traversed through the Red Sea - mainly linking Europe and Asia. The cargoes include: containership goods, oil, LNG and even livestock. Now that essentially any ship tied through some distant cousin to Israel or the U.S. is a target, shipping firms face the choice of: 1.) Paying “war risk” insurance premiums; or 2.) Re-routing…adding time (weeks), fuel, security and labor costs. While currently manageable, these costs can be expected to, at least partially, be passed along to consumers. With the Panama Canal running at significantly reduced capacity, any other hiccup - perhaps the targeting of limited air transport options - could lead to a full blown supply chain crisis. The only viable near-term respite appears to hang in the balance of a resolution/truce/ceasefire between Israel and Hamas, which seems perilous at best.

We’re paid to assess risks, and many hinge upon the upcoming November Presidential election here in the U.S. It is relatively easy to assess what to expect under a Biden win, but what about Trump? A Trump Presidency will almost assuredly lead to a much more hawkish approach to China (tariffs) and a much more adversarial approach to Europe. It appears this isn’t even on the radar of those participating in the highest market flyers that have material China exposure. For select commodities, the risks of a Trump win are the mirror image…positive price movement based upon a further movement towards more isolation and protectionism.

Takeaways: The aforementioned highlights how difficult the last mile of inflation-to-target will be and why it makes prudent sense to favor broad investment cycle rotation decisions.

SOP CHART DECK